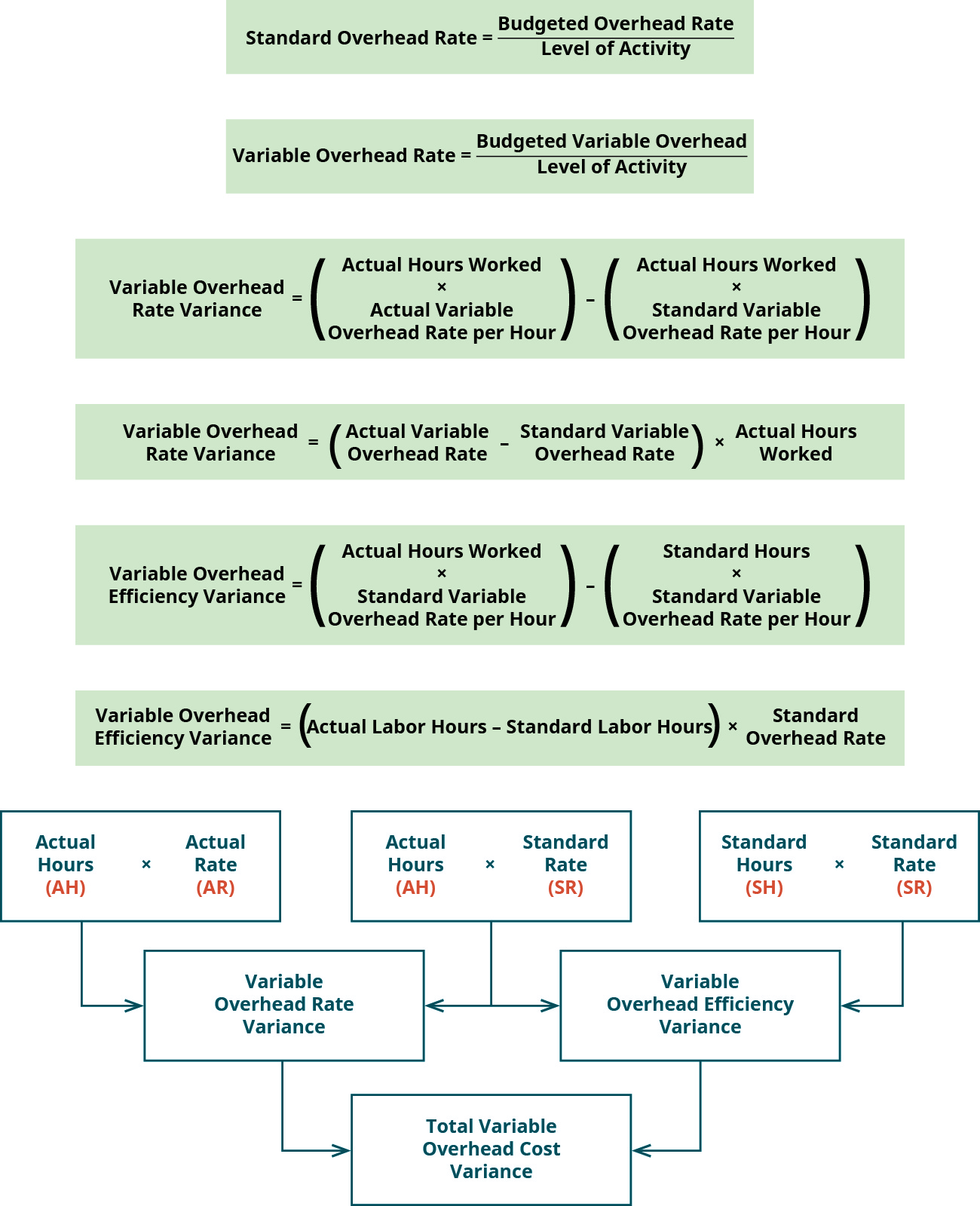

The Usage Variances Focus on the Difference Between

If it needs to pay for 1200 hours in week one its usage variance is 1000 1200 - 1000 5. Actual quantity used and standard quantity allowed for budgeted production.

2

A price variance reflects the difference between what was paid for inputs and what should have been paid for inputs.

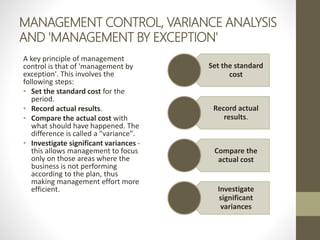

. The sum of all variances gives a picture of the overall over-performance or under-performance for a particular reporting period. Actual quantity used and standard quantity allowed for units actually produced. Actual quantity used and standard quantity allowed for actual production.

The variance is used in a standard costing system usually in conjunction with the purchase price variance. Both a and b. For example suppose a company expects to use 1000 hours of work at 5 per hour each week.

The quantity difference is multiplied by a standard price to provide a monetary measure that can be. It is one of the two components the other is direct material price variance of direct. Actual quantity used and standard quantity allowed for estimated activity.

Burden Usage and Burden Rate Variances. The usage variances focus on the difference between. The usage variances focus on the difference between.

Actual quantity used and standard quantity allowed for actual production. Fiscal Year FY A fiscal year FY is a 12-month or 52-week period of time used by governments and businesses for accounting purposes to. Quantity allowed for estimated production and standard quantity allowed for units actually produced.

The usage variances focus on the difference between aactual costs of inputs and standard costs of inputs. Variance analysis can be summarized as an analysis of the difference between planned and actual numbers. Actual costs of inputs and standard costs of inputs.

Cactual quantity used and standard quantity allowed for actual production. Profit related variances focus on the difference between budgeted and actual from BSA 1A at Aldersgate College Nueva Vizcaya. When labor is reported in Repetitive and Shop Floor Control actual labor burden costs are posted to the Burden absorption account using the burden rates.

Bactual quantity used and standard quantity allowed for budgeted production. The direct material usage variance is the difference between the actual and expected unit quantity needed to manufacture a product. The usage variances focus on the difference between a.

Usage variance is the difference in labor costs due to the difference between the actual hours reported and the standard hours earned often called an efficiency variance. In variance analysis direct material usage efficiency quantity variance is the difference between the standard quantity of materials that should have been used for the number of units actually produced and the actual quantity of materials used valued at the standard cost per unit of material. Actual quantity used and standard quantity allowed for budgeted production.

Actual costs of inputs and standard costs of inputs. Actual costs of inputs and standard costs of inputs. A usage variance shows the cost difference between the quantity of actual input and the quantity of standard input allowed for the actual output of the period.

Actual quantity used and standard quantity allowed for actual production. Rezoning conditional use permits and zoning variances come into play when someone a real estate developer a business owner or a homeowner wants to do something that is different from what the zoning laws allow. The difference between estimated inputs in a production process and actual inputs multiplied by their cost over a period of time.

Actual quantity used and standard quantity allowed for budgeted production. Efficiency variances focus on the difference between a. None of the above.

Sometimes that can mean changing the land use entirely and other times it can mean asking for an exception to a relatively minor.

Chapter 7 Solutions Cost Accounting A Managerial Emphasis

Cost1 10 Final Acn Bs Accountancy Afar001 Plm Studocu

Labor Rate Variance Definition Formula Video Lesson Transcript Study Com

Relationship Between Variances Disposing Of Variances Accountingcoach

Solved Direct Materials Usage Variances Direct Materials Mix And Yield Variances Energy Products Company Produces A Gasoline Additive Gas Gain T Course Hero

Direct Materials Variance Analysis Accounting For Managers

What Is Variance Analysis A Frontier For Analysis

Describe How Companies Use Variance Analysis Principles Of Accounting Volume 2 Managerial Accounting

Frontiers Look At The Audience A Randomized Controlled Study Of Shifting Attention From Self Focus To Nonsocial Vs Social External Stimuli During Virtual Reality Exposure To Public Speaking In Social Anxiety

Direct Materials Variance Analysis Accounting For Managers

Planning Operational Variances By Management Accounting Issuu

Agronomy Free Full Text A Critical Review On Lignocellulosic Biomass Yield Modeling And The Bioenergy Potential From Marginal Land Html

Sample And Realized Minimum Variance Portfolios Estimation Statistical Inference And Tests Golosnoy Wires Computational Statistics Wiley Online Library

Chapter 9 Standard Costing

Solved Direct Materials Usage Variances Direct Materials Mix And Yield Variances Energy Products Company Produces A Gasoline Additive Gas Gain T Course Hero

Solved Direct Materials Usage Variances Direct Materials Mix And Yield Variances Energy Products Company Produces A Gasoline Additive Gas Gain T Course Hero

Chapter 9 Standard Costing

Chapter 9 Standard Costing

Labor Rate Variance Definition Formula Video Lesson Transcript Study Com

Comments

Post a Comment